Properties

Your Trusted Company for Insurance Claims

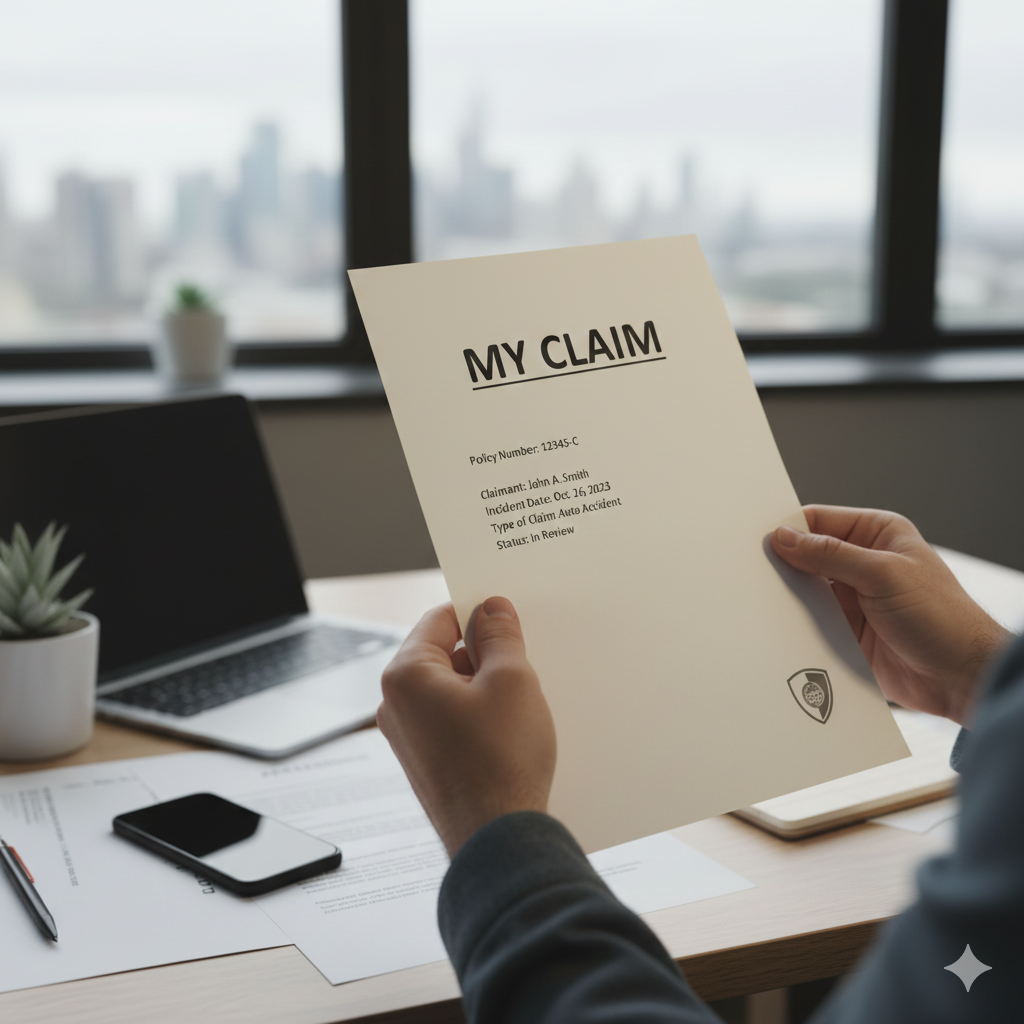

You Were Sold a Policy That Was Never What They Promised - Here's How we can try and help you Get Your Money Back

Someone sat across from you and said the words that trap millions of Indians every year: "Sir, this is just like an FD, only better." Or they promised a loan, a bonus on your lapsed policy, a job for your child, or a one-time investment. Months later the document in your hand says something else entirely - ULIP, endowment, Five, Ten or twenty-year premium term, surrender charges, non-guaranteed returns. This is not a misunderstanding. This is “Life insurance mis-selling”, and it is one of the most common financial frauds in the country.

At ClaimChase, our guidance on handling insurance mis-selling help service exists to get you out of a policy you should never have been sold, and to recover the money you have already paid. We are not an insurance company and we do not sell policies. We are on your side of the table, working to undo what an agent, a bank, or a caller did to you. This can be a trap or a target by someone to ensure that they achieve their monthly, quarterly, yearly targets

Properties

What Is Insurance Mis-Selling?

Mis-selling of insurance is the sale of a policy through false promises, hidden terms, half-truths, or pressure - a policy that does not match what you were told and often does not suit your needs at all. The moment the verbal pitch and the printed policy stop matching, you have been mis-sold.

Here is the part almost no one says plainly: mis-selling is not usually a rogue agent acting alone. It is a system built on higher commissions. An intermediary earns far more selling you an expensive endowment or ULIP than a plain term plan, so the incentive is to sell you the wrong product on purpose. An intermediary often pushes insurance because it is bundled into their targets. The person who mis-sold you was rewarded for it. Understanding that is the first step to stopping the shame that keeps most victims silent.

Do You Want To explore more services just click here

Properties

Our Services

How Insurance Is Mis-Sold - The Tactics That Actually Get Used

Mis-selling wears many disguises. These are the ones we see most often in real cases:

Sold as a fixed deposit.

The classic ULIP is sold as an FD or "guaranteed" savings plan, especially at bank counters and to senior citizens. You thought you were parking money safely; you bought a market-linked, long-lock-in product.

The loan bait.

You were promised an interest-free loan or loan approval "if you just take this policy first." The loan never comes. The premium demand does.

The lapsed-policy trap.

You were told a new policy would help you recover money stuck in an old, lapsed one. Instead you now fund two.

Fake free benefits.

A "free" health card, a tower installation with monthly income, a scholarship for your child, a job guarantee - none of which exist.

Guaranteed returns that were never guaranteed.

You were shown a minimum of 10 to 15% "assured" returns on a product whose own documents say returns are market-linked and not guaranteed.

Properties

Mis- Selling

How Banks Mis-Sell Insurance Policies to Senior Citizens

Generally there is no evidence of misselling which a customer has, most of the time the customer is being approached by a known person of the intermediary and trust is gained immediately. Since most of the people who are targets are “Senior Citizens” as they are the ones who have their Retirement savings in the bank in the form of Fixed deposits. Since they are easy targets and hence their trust is won without waste of time. Many times a 70 or 75 year old is sold a Life insurance policy without any Pre medical test or even understanding their requirements. They are often told that the policy which is sold to them carries “Attractive fixed returns” better than FD and the same can range anywhere between 10 to 15%. The senior citizens are often their easiest targets and they trust the person as he/she is most of the time an employee of a reputed bank or a reputed intermediary. They are also not given any details in writing on the insurance company Letterhead about the returns promised. The senior citizens don't even look at the policy as the same is received on their registered email id. Finally at the time of maturity when they visit banks or intermediaries, either the concerned official is either transferred to another branch of the same state or another state and it is very difficult or impossible to track the person who has sold the policy with the promise of guaranteed returns. The Dispute starts now and the “Misselling” is detected at the time of maturity only in most of the cases as the policy was purchased on trust as the bank official or the intermediary had convinced very sweetly to buy the policy.

Another case

- Forced bundling. Insurance quietly attached to a loan, locker, credit card, or a new bank account - sometimes with a premium deducted before you even knew.

- The wrong product for your life. You needed simple, high-cover term insurance; you were sold a costly endowment because it paid the seller more.

- Hidden charges and pressure. Surrender charges, administration fees, and premium-payment terms were never explained, and you were rushed to sign before you could read.

If any of these sound like your policy, you were not careless. You were targeted.

Properties

Why Choose Us

The Evidence That Wins Your Case - Gather It Before It Disappears

Once the free-look period is gone, a mis-selling claim is won or lost on proof. Here is what most people don't realise: much of the evidence that convicts the insurer already exists - in their records and in your phone - and it fades with time.

Your side of the sale.

WhatsApp chats, SMS, and emails with the agent. The handwritten “returns chart” or benefit sheet they drew for you. Any brochure or screenshot showing the promise.

The insurer's own records.

By law, the sale should be backed by a proposal form, a benefit illustration you signed, and in many cases a pre-issuance verification or welcome call recording. We help you formally demand these – because the insurer’s own documents often prove the policy was never explained.

The mismatch.

A clear, side-by-side of what you were promised versus what the policy document actually says – the premium term, the surrender value, the charges, the market risk, the non-guaranteed benefit.

34

Years Of Experiences

Properties

OUR Every Steps

How ClaimChase Guides you on recovery of your Mis-Sold Policy

We built our insurance mis-selling resolution process to be simple for you and hard for the insurer to ignore. You hand us the mess; we handle the fight.

Review and diagnose.

Share the policy and your story with us. We check your free-look status first, read the actual policy terms, and tell you plainly whether it is mis-selling and what recovery looks like - before you spend anything.

Build the case.

We assemble your evidence, demand the insurer's proposal form, benefit illustration, and call records where they exist, and draft a factual, well-documented mis-selling grievance that states exactly what was promised, how the policy differs, and the relief you are owed - cancellation, refund of premiums, or compensation.

Escalate and resolve.

We will guide you on the process where one can f/up and also ensure that Justice is delivered to you at the earliest.We keep pushing until you get a fair resolution, not a token offer.

You stay informed at every stage - in plain language, with no jargon and no chasing.

Properties

Expert People

Meet the Experts Fighting for Your Insurance Rights

ClaimChase is built by insurance industry insiders who have spent decades on the insurer's side - and now use that knowledge exclusively for policyholders. When you work with us, you are not dealing with a call centre. You work directly with a claim specialist who knows your case.

Properties

Talk to a Claims Expert

Who We Help

Our mediclaim claim assistance is for anyone facing a health insurance claim - individuals, families on a floater policy, senior citizens, and those supporting an unwell relative through hospitalisation. Whether the claim is a routine reimbursement or a denied high-value hospitalisation running into lakhs, we handle it with the same care and the same goal: the full amount your policy is meant to pay.

1

Submit Your Claim

Start by submitting your insurance claim with the required documents. We’ll guide you through what’s needed for a smooth and fast process.

2

Claim Analysis

Our team of experts will carefully review your case, verify the claim, and coordinate with the insurer to ensure accurate evaluation.

3

Support & Resolution

We’ll keep you informed, answer your queries, and work toward a timely settlement—ensuring you receive the compensation you deserve.

Properties

Testimonials

We are very happy for our

client’s reviews

I wanted to extend my heartfelt thanks for Hemant's sir invaluable support in recovering the claimed amount from Star Health Insurance Company. His assistance was crucial in resolving this matter efficiently and effectively. I truly appreciate dedication and effort of his team in navigating through the process. My claim was from Jupiter Hospital Thane and Sushrut Hospital Chembur. Claim chase helped me to get almost 90-95% of the claimed amount. Thank you once again for your outstanding support. I highly recommend service from Claimchase Company.

Omkar Pingle

Professional

I had ordered a watch from a reputed company through an online portal. I was shocked to see an empty box when I accepted the delivery. Even after my rigorous pursuit there was no response. Finally, Claimchase came forward to help me and fought the case and I got my 100% refund of Rs. 24,000/- within 4 months.I thank their entire team from the bottom of my hea

laxmi dakua

WordPress Developer

I had ordered a watch from a reputed company through an online portal. I was shocked to see an empty box when I accepted the delivery. Even after my rigorous pursuit there was no response. Finally, Claimchase came forward to help me and fought the case and I got my 100% refund of Rs. 24,000/- within 4 months.I thank their entire team from the bottom of my hea

Pradeep Shukla

Interior Designer

My Mediclaim claim was rejected by Pvt insurance company for Rs.67675 and claimchase and its team fought at Belapur court and I received Rs.118000 including interest and penalties. I received this amount after 2years. I thank Mr. Sagar and Claimchase company for fighting my case and giving my claim. Thank you for your service

Karan Patil

Engineer

Properties

yOUR dOUBTS

Frequently Asked Questions

What is insurance mis-selling?

Insurance mis-selling is when a policy is sold to you through false promises, hidden terms, or pressure - for example, a ULIP sold as a fixed deposit, insurance forced with a loan, or guaranteed returns promised on a market-linked product. If what you were told does not match your policy document, it is mis-selling.

Can I cancel a mis-sold policy and get my money back?

Yes. Inside the free-look period - usually 15 to 30 days of receiving the policy - you can cancel and get a refund with minimal deductions. After that window, you can still seek a refund by filing a mis-selling grievance and escalating to appropriate grievances authority, the Insurance Ombudsman, or the consumer courts, supported by evidence.

My free-look period is over. Is it too late?

No. It is harder, but not too late. After the free-look window, the case rests on proof - your chats and brochures, the mismatch between the promise and the policy, and the insurer's own proposal form and call records. Many post-free-look cases are still resolved through the insurance grievances department, ombudsman and or consumer courts. We help you build and pursue that case.

How long do I have to complain about mis-selling?

Beyond the free-look window, complaints can generally be raised within a few years, and the clock is often counted from when the mis-selling was discovered, not only from the date of purchase. If an insurer claims your case is time-barred, that is frequently worth contesting rather than accepting.

What evidence do I need for a mis-selling complaint?

Anything that shows the promise and the mismatch: WhatsApp and email with the agent, brochures, a written returns chart, and the insurer's own proposal form, benefit illustration, and welcome-call recording. We help you gather and demand these.

How much do your mis-selling services cost?

Our engagement is straightforward and discussed upfront during your free consultation. You will know exactly how we work before you commit - and remember, no genuine service will ever ask you to pay a "fee" or OTP to release a refund.

Properties

Latest News & Tips

Resources to keep you informed.

Insurance is a means of protection from financial loss which innei exchange

for a fee, a party agrees to guarantee another party